Financial Impact of Big Ticket Items

Published November 2017

Written by Shawn Yap CFP

Big ticket items are highly-priced consumables that we spent our hard earned money on. Some are inevitable while others are choices. In this article, we discuss three of the biggest financial commitments in Singapore.

Home

Home loan will be the biggest liability for many home owners. Home loan is a ‘double-edged sword’ as it can provide positive and negative leverage effect. While Singapore property (whether HDB or Private) had appreciated strongly, past performance is not an indication for future performance. Home owners should focus on managing their home loan for prudent financial management rather than to hope for the property price to appreciate like in the past.

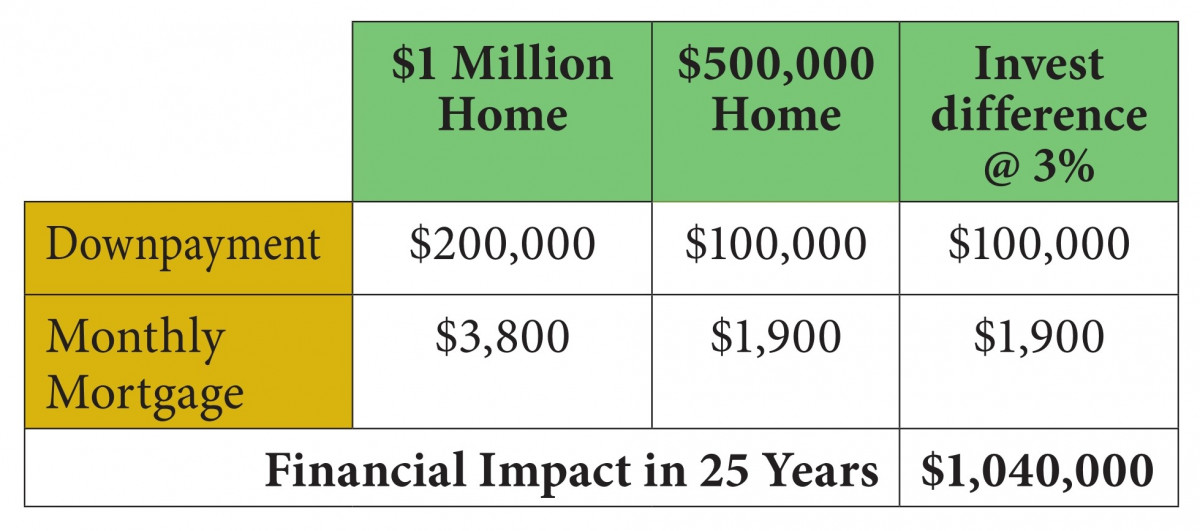

For Singaporeans and permanent residents, the use of the Central Provident Fund (CPF) has aided in the ownership of homes. Unfortunately, some home owners have exhausted their CPF and risk compromising the primary objective of CPF - retirement funding. With a median lifetime income of $3 to $5 million, the allocation towards the purchase of a home could significantly affect the owner’s nest egg. Now, let us find out the difference between buying a $500,000 versus a $1,000,000 home.

Assuming a downpayment of 20%, interest rate of 3% and a loan period of 25 years, the table shows the huge difference of more than $1 million!

Car Ownership

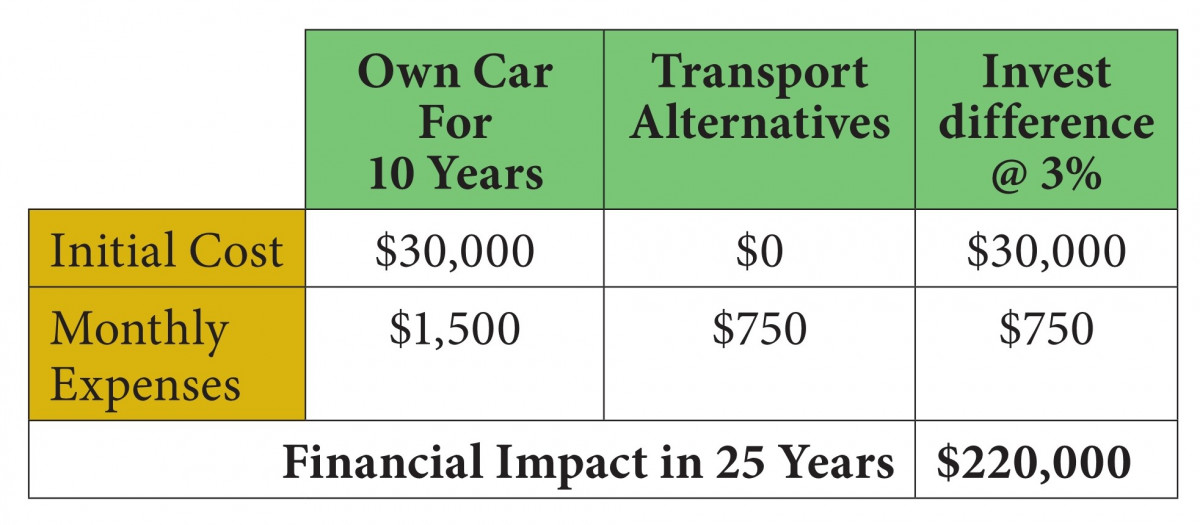

Another big ticket item is the cost of car ownership. Singapore is notoriously known for its high costs of car ownership in the world. It is enlightening to see the responses of Hollywood stars when told the prices of cars in Singapore. They are multiple times that of the States. In addition, cars with higher horsepower usually come with higher insurance and road tax. Car buyers commonly gauge the affordability of a car based on the downpayment and monthly instalment. Many failed to calculate the total cost of car ownership and compare it with other alternatives. The real costs should include petrol, parking, ERP, tax, insurance, maintenance, consumables and the occasional “cons” by car mechanics. Assuming a car price of $100,000, downpayment of 30%, interest rate of 2.5% and a hypothetical loan term of 10 years, the true cost of car ownership is about $1,500 per month. The alternatives to car ownership are bus, train, taxi, cycling, car sharing and ride-hailing platforms. Grab and Uber have made transportation more convenient to consumers. Now, anyone can be chauffeured by a “private” driver. A mixture of the various transport alternatives could cost much lower than car ownership.

You can see from the table that the long term consequence (25 years) of owning a car for just 10 years is more than $200,000. Imagine how much another 10 years of car ownership would reduce your retirement fund by.

Education

We have gone pass the era where parents are proud of their children who wear the square academic caps which indicate a high level of education that in turn secure a good future ahead. Graduates are rare in those times. Today, having a bachelor’s degree is not that uncommon. The value of a bachelor’s degree has been called into question where technological disruptions are happening in almost every industry. Bill Gates, Steve Jobs and Mark Zuckerberg are all school drop-outs. Jack Ma was rejected 10 times by Harvard University. The idea here is not to quit school but to examine the cost and value of tertiary education.

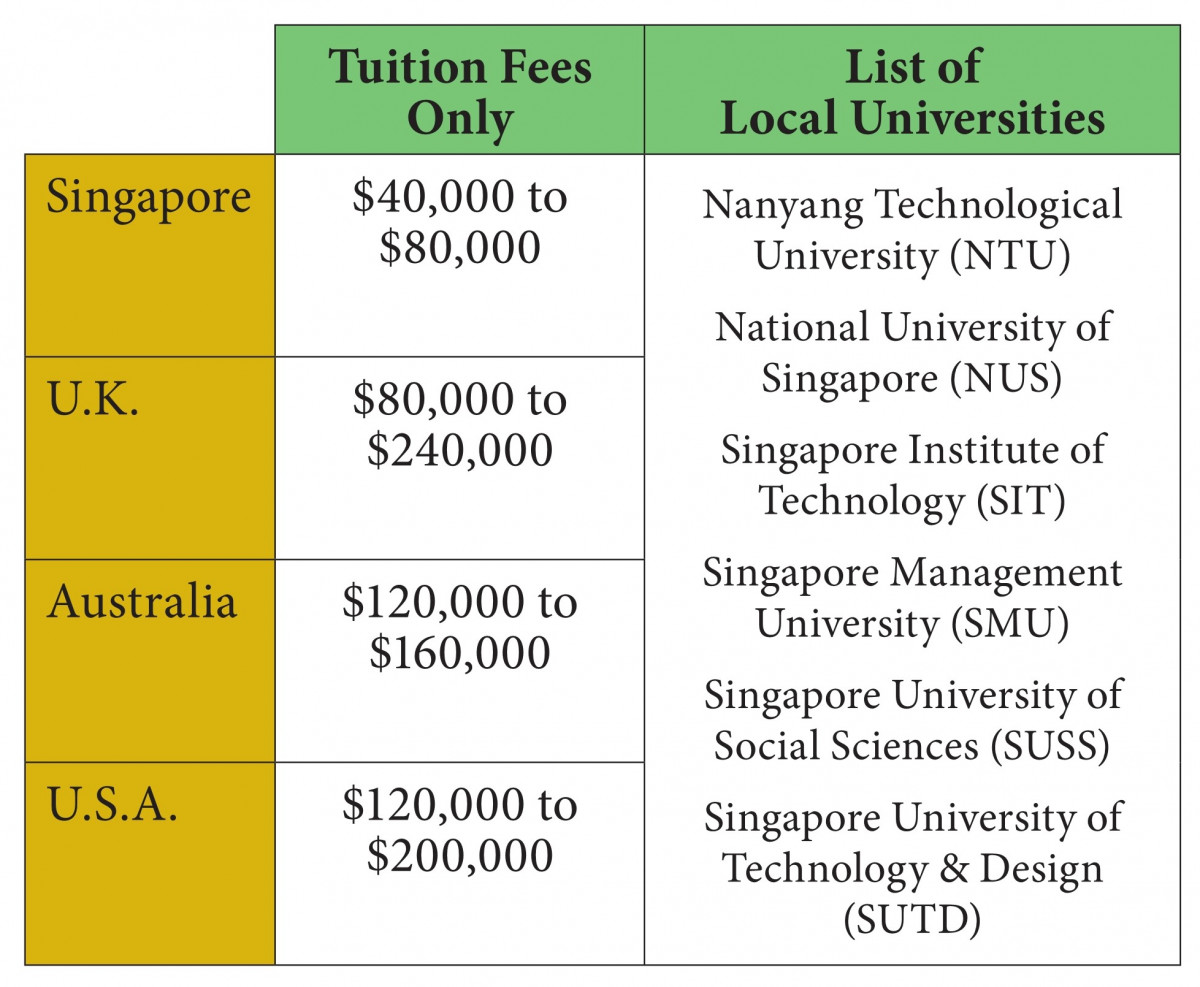

With 6 local universities providing courses in different fields, there is little need to venture overseas to get a tertiary education. The difference might just be an experiential one. Moreover, an overseas tertiary education cost several times more than a local university. With the internet, distance learning and twinning programmes have seen increasing popularity. Students need not travel so far to another country, spending extra money on lodging and food. Having an overseas degree also does not mean a higher starting salary. In fact, it takes longer to breakeven on education costs. Even though this is the case, there is a well-known saying that it is not what you know but who you know. Studying in prestigious schools may connect you personally to people in high places if you network diligently. Social media like LinkedIn are trying to replicate that but nothing beats a face-to-face communication. The table shows the approximate difference between local universities and overseas universities. Note that specialised courses like medicine and tuition fees of elite schools cost much more.

In conclusion, we should earn enough money in our lifetime for retirement. The key is to choose our expenses wisely. The first 2 tables are illustrated using a conservative rate of return at 3% per annum. The difference is even greater when the returns are higher.

This article first appeared in the November 2017 issue of Financial Planning magazine published by the Financial Planning Association of Singapore (FPAS).