Power Budgeting

Published November 2008

Written by Shawn Yap CFP

This article tells you how to create a yearly personal or family budget.

"The Millionaire Next Door” is one of the most comprehensive studies ever done on America’s wealthiest and how they did it. According to the study, the top quartile of wealth accumulators spent an average of 100.8 hours a year (8.4 hours per month) planning their finances.

Do you have a yearly personal or family budget? If not, this article can help.

Personal budgeting tends to carry negative connotations among many consumers. It seems complex and time consuming and many feel that they lack the knowledge or skill to create a personal budget. Some even hold beliefs like, “I don’t have enough money to budget.” Or “I like to enjoy the finer things in life.”

Budgeting actually ensures that one has sufficient money for everything, enabling one to fulfill short, medium and long term goals. A personal budget allocates money towards expenses, loans and savings; and is the foundation to achieving your financial aspirations. You may have heard wise sayings like, “Pay yourself first” or “Never spend more than you earn”.

It seems like common sense. But common sense is rarely common practice.

Begin with the End in Mind

Think about these questions: What do you want to achieve? Who is involved? Why is this goal important?

Examples of goals and dreams that some of us have are:

- “$20,000 to establish a standby fund for any emergency within 6 months”;

- “$500,000 for my daughter’s university tuition fees and living expenses in the United States when she turns 18 so that she can start work with a basic academic qualification”;

- “$3,000,000 for my financial independence so that I can retire to enjoy my desired lifestyle with my loved ones in 20 years”.

Once you have your goal in mind, we can budget for it.

Analyse Your Current Situation

There are two types of budgets: the Net Worth Budget and the Cash Flow Budget.

The Net Worth budget is used to evaluate how much of your resources can be used to achieve your financial goals. Take an inventory of what you have now. On a piece of paper, create two columns.

On the left column are sleeping assets, working assets and lifestyle assets. Sleeping assets are money for emergencies or planned expenditures. Working assets are investments for growth over the medium to long term. Lifestyle assets are properties that do not appreciate or are for usage or consumption purposes. On the right column are liabilities consisting of all outstanding debts.

Assets minus liabilities equals net worth. Net worth is a measure of wealth. Most likely, only sleeping and working assets can be used to meet your financial goals.

First Things First

The Cash Flow budget is most commonly used for personal budgeting. When budgeting for cash flow, there are two vital guidelines to keep in mind.

- Use less than 35% of your income to service long-term loans and

- Regularly save more than 20% of your income

Before You Budget

Do your Risk Management (less than 10% or 15% of income)

There’s nothing to budget if there’s no money. Any crisis that can delay, suspend, reduce, or even stop income must be insured. Protect the source of your wealth at all cost! Use less than 10% (15% for sole bread winner) of your income to insure more than 10 years of your income.

Set up an Emergency Fund (3 to 12 months of outflows)

Emergencies, such as temporary unemployment, can disrupt your finances. Unforeseen purchases or expenses may arise from situations such as repairs or replacements. Most advisers advocate between 3 to 12 months of expenses as a buffer. Your emergency fund must be easy to withdraw with minimal or no capital loss.

Annual Budgeting

One common mistake in budgeting is to do it on a monthly basis, forgetting to take into consideration the cash flows taking place on a yearly (or more) basis like bonuses, taxes, etc.

You can overcome this by creating a spreadsheet to track your cash flows monthly from January to December, for an entire year. You will notice which months are “drier” (fewer expenses) or “wetter” (more expenses).

List each item on the left side and label the months on top. Group items according to the following categories:

Income (inflow)

Include all forms of income. Examples: salaries, bonuses, businesses, director fees, profits, allowances,rentals, interests, dividends, alimonies, pensions, inheritances, annuities, insurance cash backs, etc.

Savings (outflow)

Include all forms of savings and investments. Examples: Save As You Earn plans, regular savings programs, investment-linked policies, endowments, shares purchase schemes, etc.

Loans (outflow)

Include all forms of loans. Examples: properties, vehicles, renovation, studies, interest-free, overdrafts, policies, personal, etc.

Expenses (outflow)

Include all forms of expenses. Examples: family, children, parents and personal maintenance, insurances, transport, utilities, groceries, services, education, subscriptions, memberships, entertainments, recreation, hobbies, vacations, luxuries, shopping, charities, tithe, road, income & property taxes, etc.

Net Cash Flow

Deduct Savings, Loans and Expenses from Total Income to get your Net Cash Flow.

If you have a negative Net Cash Flow, then either you’re in debt or you’re using your past savings or cash reserves to finance your current lifestyle. This may be unhealthy over time. If you have a positive amount, you can then choose to spend more or save and invest more towards your short, medium and long term goals.

This clarifies your overall cash flow management and gives you a sense of control over your money. Remember that clarity is power.

Post-Budgeting

Budgeting isn’t rocket science, so do allow a few months for it to work. Have fun with it. Track your cash flows with graphs and look at how your money flows from month to month.

If you think you can increase your savings by increasing income, think again. One of the best known laws of wealth accumulation is Parkinson’s Law. Popularised by bestselling author and speaker, Brian Tracy, the law states that no matter how much you earn, you will tend to spend slightly more than the entire amount.

Consequently, there are only two ways to increase savings. The first is to increase income and maintain expenses. The second is to maintain income and reduce expenses. Neither are easy. That’s why few achieve financial independence.

Small Change Big Difference

Generally, any individual or organisation will need to manage money.

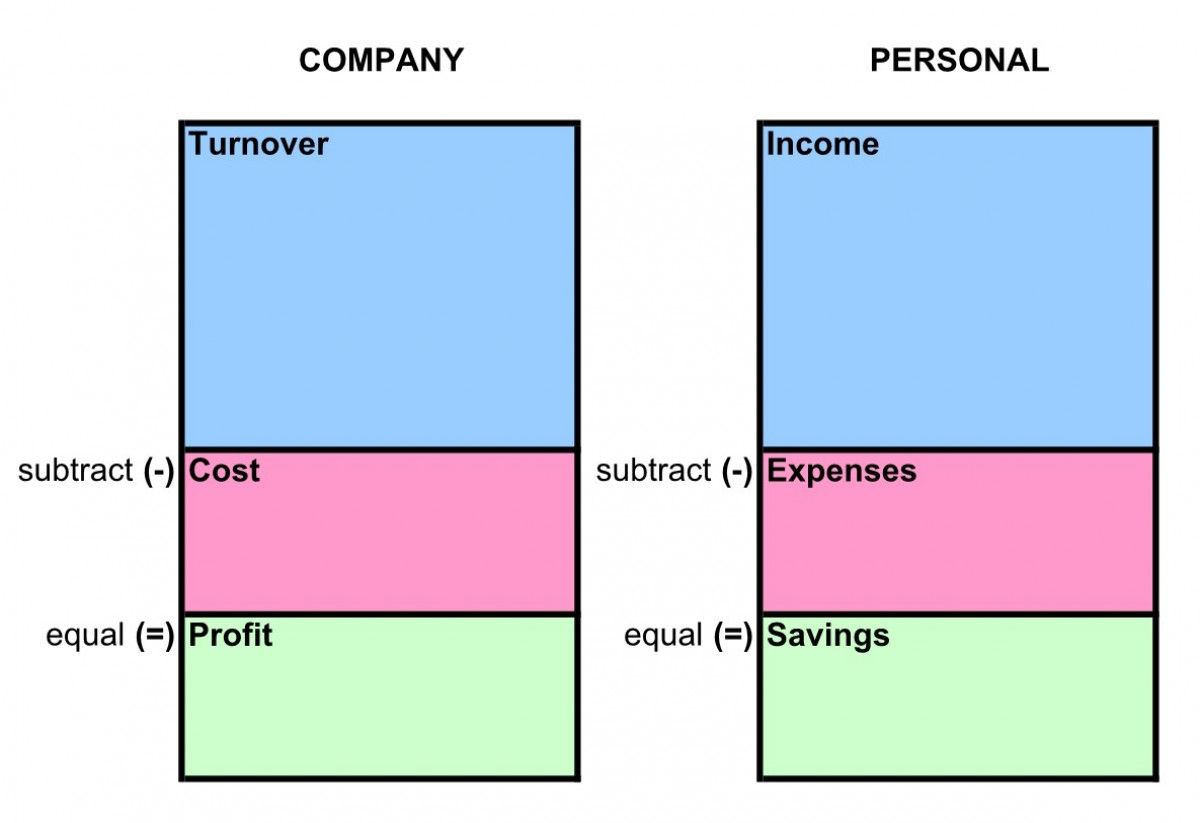

Profit is what you get after subtracting cost from revenue. This is an undeniable fact of business. Similarly for a personal cash flow statement, savings is what you get after subtracting expenses from income. It seems fine because this is the most common type of calculation done by many people. However, this is the main reason why most people are financially “poor”.

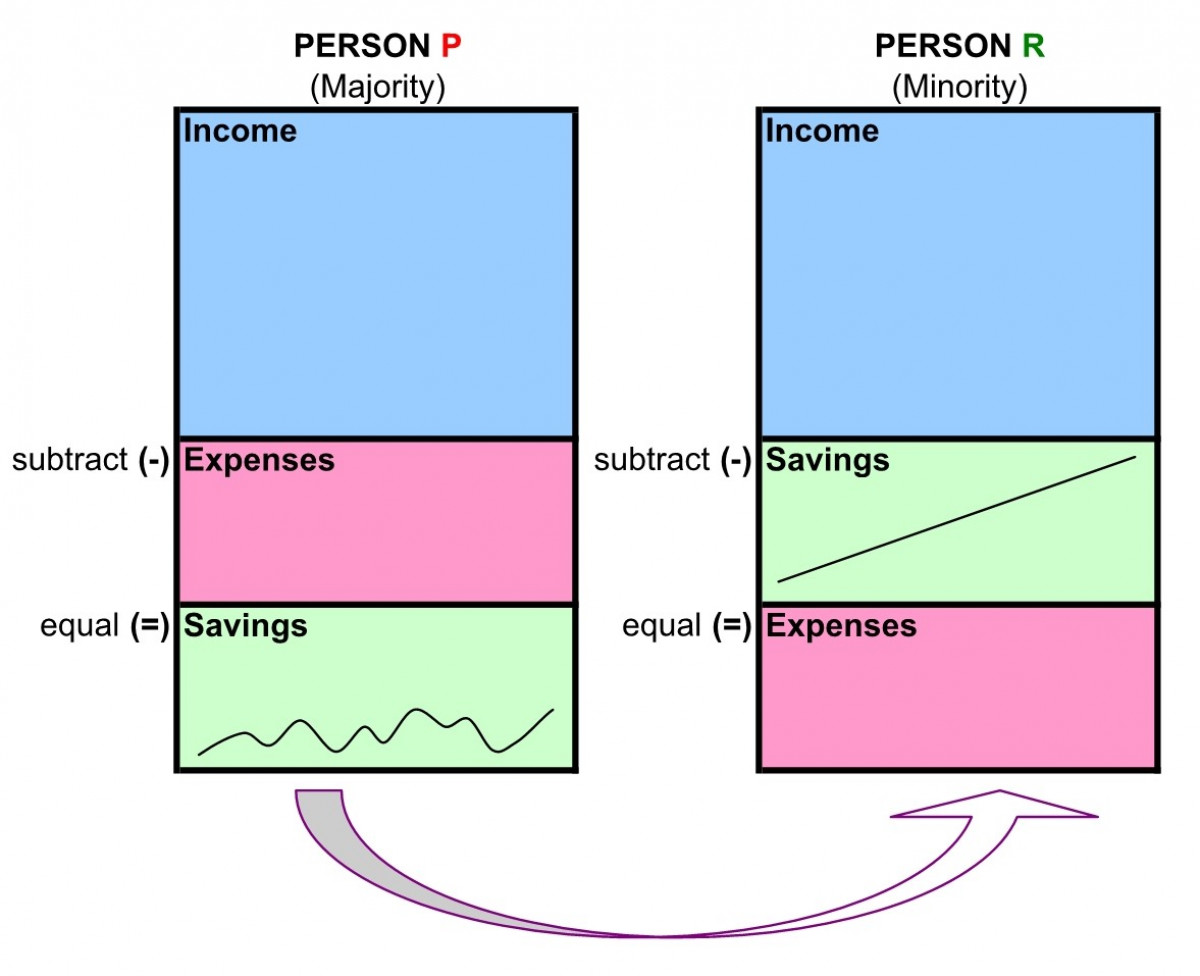

Unlike a company, a person can switch the sequence of the cash flow statement. Person P spends on everything then saves, usually with little left. Person R saves first then spends the rest. Simply by changing the sequence of your budget management, you immediately create an automatic and disciplined system to accumulate wealth. Then you can spend the rest of your money guilt-free.

So do you “Pay yourself first”?

Savings vs Investments

Saving and investing always work hand in hand when accumulating wealth. Over-saving is a situation where a person saves a lot with little or no investment resulting in an overly inflated emergency fund which results in the value of money (and wealth) shrinking over time.

The opposite scenario is a person who saves little and expects a high rate of returns from investments. There are three basic determinants of investment success: time, money and rate of return. Usually, we can’t control the rate of return. If you save little and expect a high rate of return, there is a risk of not meeting your goals. If you invest later, you miss out on the effect of compound interest, sometimes referred to as “the most powerful force in the universe.” If you save more, invest early and expect a reasonable rate of return, there is a good chance of achieving your goals earlier.

Which is your best bet?

This article was published in the iFast Insight magazine in 2008 Q4.