Financial Planning for First-time Parents

Published May 2015

Written by Shawn Yap CFP

Your first baby is not your only major milestone in your life. In fact, it can change your life significantly. Not only do mummies have to cope with the demands of pregnancy, but daddies also develop a condition called Couvade Syndrome, also known as sympathetic pregnancy, where the males experience the same symptoms and behaviours of expectant mothers. As parents, we are often anxious to provide the best for our children. However, in our fast-paced modern society, both time and money fast become scarce resources. The purpose of this article is to help you to navigate through some of the vital issues of new parents.

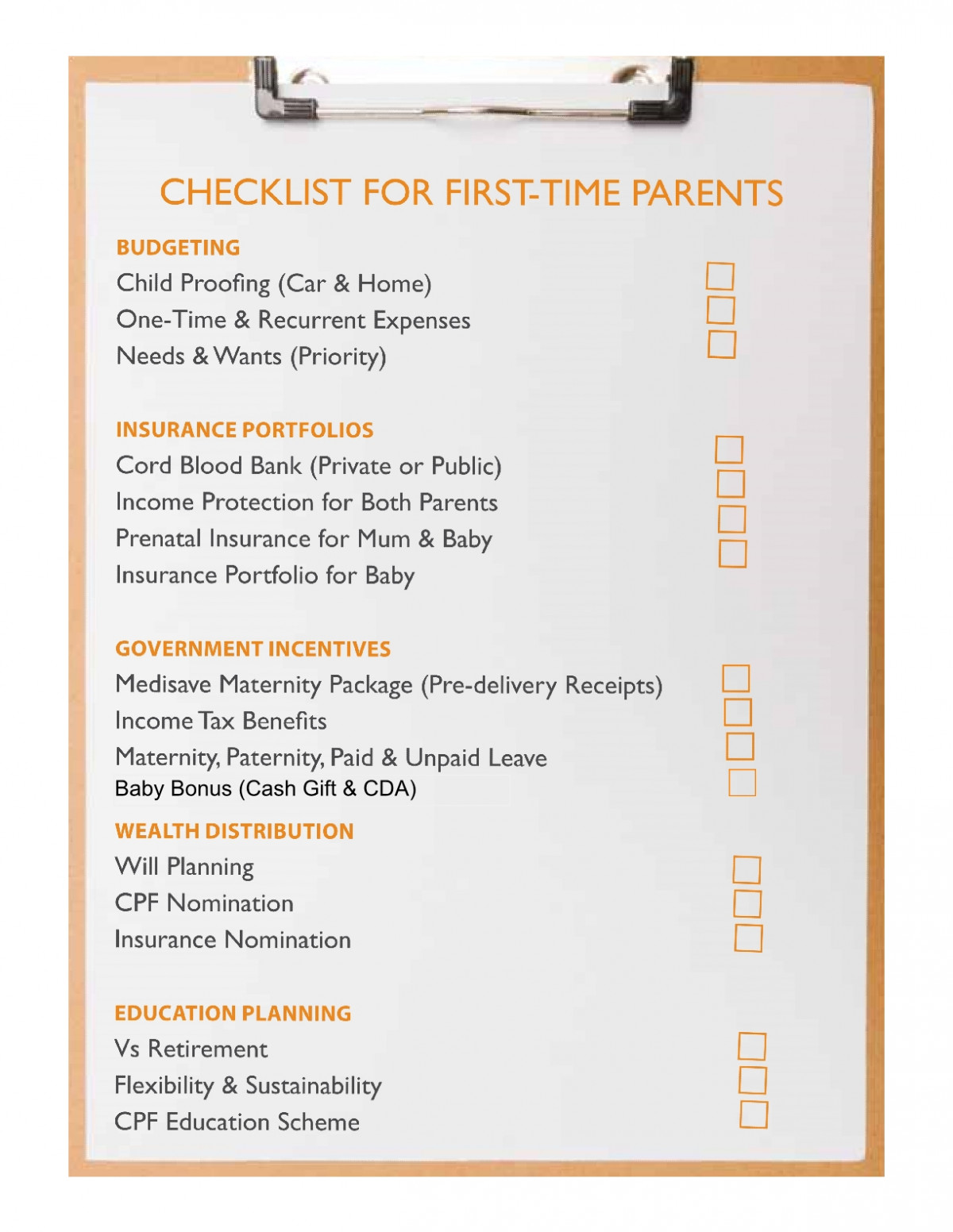

Budgeting

Cash management is one issue you may be concerned about. Baby expenses can result from an endless shopping list and could make a dent in your wallet without you noticing. Almost everything looks cute in small sizes so be mindful of what you purchase. Babies and children grow up very fast so they outgrow everything in the blink of an eye, especially clothes, toys and infant furniture. Always try to get used items when you can. Do your best to differentiate between needs and wants. Using a cooking pot or a brand new food steamer rather than a bottle steriliser can also save you some bucks. Child proofing your car and home is a must-do. There have been cases of young children falling out of windows. So remember to look into safety measures such as window grilles. If you are shopping for a car seat, look for models that can last as long as possible. Some models are designed only for babies and some are configurable from newborn up to toddler or older depending on their height and weight.

After delivery, confinement assistance and food are very important to mummies. Going forward, there will be more recurrent expenses such as diapers, milk, infant/child care, etc. Use two categories for your budget list, one for the one-time expenses and the other for recurrent expenses. Then go through it and prioritise them. You might be surprise to find possible savings here and there.

Insurance Portfolios

Before we go into insurance, you may want to look into banking your baby’s cord blood. This is considered a form of insurance that you can only “activate” during delivery. You can either store it privately or donate it to save lives.

Now, imagine you are travelling with your child in an airplane. Suddenly, the aircraft loses pressure and oxygen masks drop from the ceiling. What do you do first? Do you put on the mask for your child or on yourself? Of course, you would put it on yourself first so that you will remain conscious to take care of your child. Therefore, parents should always insure themselves adequately first before the child. It’s just like insuring the goose that lays the golden eggs. I have seen some babies who have more insurance coverage than their parents. What if something happens to the parents, the income providers? None of the child’s insurance plans can provide even the basic necessities. Let’s assume that your own insurance portfolio is taken care of and you want to determine how much more income protection you need to ensure your child’s financial security. Just ask yourself how much living and educational expenses your child will need every month. If we take $1,000 a month, that would be $300,000 for the next 25 years excluding tertiary education! This shortfall can be easily covered with a low-cost term protection as our children only need our support until they they are financially independent.

So, how about life coverage for children? Any life insurance bought on the child’s life can be treated as a gift to the child by securing the low premiums throughout adult life. Most importantly, any insurance payout due to the child’s disability or illness can come in handy because the parents would have a choice to stop working to support the child both physically and emotionally for a period of time without financial strain.

According to the Ministry of Health statistics, the group with the highest rate of hospital admission for children is from zero to four years old. Hence, medical plans that cover hospitalisation and surgery are like breast milk to a baby. It is better to purchase this early because of the strict health requirement compared to other types of insurance, even for adults. One of the main causes of children’s hospitalisation is accidents and injuries. Nowadays, insurers have included common infectious diseases such as hand-foot-mouth and even dengue fever in their Personal Accident plans specially designed for children.

The final category is perhaps the most interesting. That’s the prenatal insurance that covers a comprehensive list of pregnancy complications for mother and congenital illnesses for baby. But the most valuable part of the plan is that the life assured of the insurance can be changed to the child upon delivery without any evidence of good health. Do take note of the transfer period for this guarantee.

Government Incentives

Other than the Cash Gift of the Baby Bonus, the Children Development Account (CDA) comes in very handy to stretch your dollar. The government will match your savings dollar-for-dollar up to a cap depending on the birth order of the eligible child. It is like an investment that gives you a 100% guaranteed return. You cannot get this anywhere else! Although the monies cannot be withdrawn in cash, it can be used to pay for expenses incurred in many approved institutions and programmes such as education and healthcare including child care. Do not worry about unused balance in your child’s CDA as the remaining monies will be transferred to the Post-Secondary Education Account (PSEA). You may continue to contribute to the PSEA and still receive the Government’s matching contributions subject to the contribution cap. The funds in the PSEA can be used to pay fees at approved institutes and programmes even for the child’s siblings. Subsequently, any unused funds will be transferred to the account holder’s CPF Ordinary Account.

For the Medisave Maternity Package (MMP), do remember to keep all the receipts of your pre-delivery medical expenses such as consultations and ultrasound for withdrawal up subject to a limit. On top of this, Medisave grant is also deposited into your baby’s CPF Medisave Account.

There are three income tax benefits to reduce your tax obligations. They are Qualifying Child Relief (QCR), Working Mother’s Child Relief (WMCR) and Parenthood Tax Rebate (PTR). The QCR can be used by one parent only and the WMCR allows a proportion of a working mother’s earned income to be exempted from income tax. The PTR can be shared between you and your spouse.

As for paid leaves, working mothers have their Maternity Leave while working fathers have their Paternity Leave. Fathers can also share a limited part of their spouse’s Maternity Leave subject to the agreement of their spouse. In addition, you and your spouse are each eligible for Paid Childcare Leave and Unpaid Infant Care Leave.

Out of all the above, only the QCR is available to all income earners while the Medisave Maternity Package is available to Singapore Citizens and Permanent Residents only.

Education Planning

First and foremost, remember this: you can take a loan for education but not for retirement. And relying on children is not a prudent retirement plan.

Tertiary education is another big ticket item. The total cost varies depending on where the school is. Tuition fees for medicine and dentistry cost more. Sending your children overseas will also incur more expenses like living costs. Make sure that the education fund is ready before the beginning of your child’s academic year. I have come across a couple who bought education plans for each of their three children, and all of them matured up to six years too late.

The term “Education Plan” was coined by the financial industry to market plans for accumulation. What if you rely on a single plan for education and it “fails” to deliver the returns? Therefore, you need not allocate a specific plan just for education. Be it bonds, endowment, unit trusts, stocks or property, any instrument can be for education as long as you have a diversified growth portfolio. By the time your child needs it, you can decide which asset class to draw from.

For equity-based instruments like unit trust and stocks, remember to lock in the profit at least five years before your child enters university to protect the fund from any downside. For insurance-based plans, the projected values can be subject to change. The key merit of using insurance-related instrument is that if the payor (parent) meet any crisis (death, disability, disease, etc.), the accumulation will automatically continue till the end of the tenure. Of course, the certainty of the funding can be done in other ways, like insuring the payor for the maturity amount.

Occasionally, parents would use their CPF Ordinary Account for their children’s education subject to limits. Under the CPF Education Scheme, the child has to repay the loan to the parent in cash, not CPF, including interest based on the prevailing rate.

There is no best plan. Every choice has its inherent advantages and disadvantages. The most important thing to bear in mind is the flexibility and sustainability of your strategy. What if you need to stop the plan due to unforeseen circumstances such as pay cut or change of industry? Avoid rigid strategies that commit you over the long term. Do start early to take advantage of the effects of compounding and reduced risk with a longer time horizon.

Conclusion

What we have discussed form only part of the full spectrum of personal finance, so taking a wholesome approach towards wealth management is crucial. It’s always best to review your overall financial position because the arrival of a baby could change your financial circumstance quite drastically. Your financial planner should be able to customise a holistic strategy that will match your unique situation to fulfil your financial aspirations.

Last but not least, avoid investing too much on your first child. You will not know if or when the second child is coming. Children may be financial liabilities but parenting is priceless. Happy Parenting!

This article first appeared in the May 2015 issue of Financial Planning magazine published by the Financial Planning Association of Singapore (FPAS).