Managing Healthcare Costs

Published May 2014

Written by Shawn Yap CFP

According to GlobalSurance, a leading international health insurance expert, the premium inflation of some private medical insurance can reach double digits. In 2013, MediShield premiums increased by up to 100% and Medisave-approved Integrated Shield plans increased by up to more than 60%.

Trends

According to the Ministry of Health, the highest hospital admissions are children from zero to four years of age and seniors above 55. Therefore, it is vital that medical insurance is the first insurance plan that a new born should have. Another reason is that any medical conditions might be excluded permanently if the child is not insured early. Among all types of insurance, medical insurance has the strictest health requirements causing it to be the most difficult insurance to purchase. Once you have any ailment, any conditions caused directly or indirectly by it may be excluded for life. Unlike life insurance plans, they cannot be included even with extra premiums. Therefore, it is crucial to buy as early as possible and make sure it is manageable till old age.

For seniors, hospital admission rate increases by more than 30% every five years from 55 years old onwards. Healthcare costs are expected to continue its uptrend for years to come. In fact, the pace of inflation for healthcare is one of the fastest across all items. This is due to demographics and longevity. In 2030, the old-age support ratio will drop to two from the current six and the number of seniors will triple. Singapore ranks within the top five in the world for life expectancy. Longevity does not mean good health. Rich men’s diseases such as diabetes, high blood pressure and high cholesterol levels are so common that they are touted as the new norm.

Work On What You Can Control

MediSave-approved Integrated Shield plans are good enhancements over the basic MediShield as they provide as-charged basis with high sub-limit, lifetime cover and guaranteed renewability. Note that there is an annual MediSave withdrawal limit for Integrated Shield plans. As you grow older, you have to pay part of the premiums by cash.

Contrary to life insurance premiums where the premiums are mostly constant, the premiums of medical plans are not. Premiums are not based on entry age but will increase according to the relevant age band. The stated premiums are based on today’s value. It would be wise to choose a structure assuming you are on the plan forever because changing the plan or company gets more uncertain as you age because of health conditions.

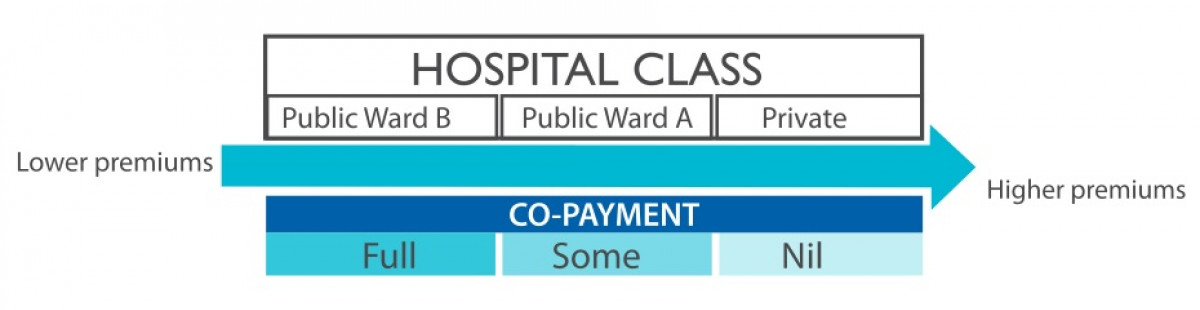

Referring to the figure, there are two variables that determine the premiums you pay: Hospital Class & Co-Payment. Hospital class is usually classified into three types: Private hospitals, Public hospitals Wards A and B. Some companies only have two types: Private and Public. This means that you are paying the same premiums regardless of whether you stay in Ward A, B or C. Co-payment is the deductible and/or co-insurance you pay before any reimbursement for claim. The full co-payment is the first S$1,500 to S$3,500 plus 10% of the remaining medical bill. In a Towers Watson survey report, one of the top three significant factors driving medical costs is overuse of care. Generally, patients would exercise more prudence with some co- payment in place. Therefore, the premiums of medical plans with zero co-payment also known as first-dollar claim may rise faster than those with a higher co-payment.

To manage future premiums, one can choose a flexible structure that can be downgraded by hospital class or co-payment, if not both. The fundamental concept of insurance is to cover catastrophic costs, not small medical bills which could be paid directly from the MediSave account.

Insurance companies are important, too. The premiums for medical insurance are similar to car insurance except that it based on a specified age group rather than an individual.

For car insurance, your premium increases once you are at fault in an accident. For medical insurance, it is based on the claim experience of that age group. Companies that include more frills and insures those with existing medical conditions because of more lenient underwriting requirements may also face higher premium increases in the future. The insured pool size matters too. If the pool size is large, an average premium is likely. If the pool size is small, it depends on claims experience on that particular pool. Higher claims would lead to higher premiums.

Caution

Note that not all medical costs would be covered. Due to technological advancement, some special medication can cost S$50 a pill and are not approved as an allowable claim. For a holistic healthcare portfolio, a whole life major illnesses cover and a long-term care protection (e.g. ElderShield) are recommended.

If you have any medical conditions, apply at different insurers and pick the best deal with the least exclusions. For example, even if you are faced with any exclusion because of high blood pressure and high cholesterol, you should still be covered for accidents and cancer. For those who already have an existing plan, do be extra cautious when attempting to change to another insurer. The new insurer would most likely exclude any pre-existing conditions even if your previous insurer covers them. You have to weigh the pros and cons very carefully.

Most employees would be covered under their employer’s medical plan. Never rely solely on them as they usually have multiple sub-limits and are not portable. The company owns the plan, not you. If you change company, the new company may not insure you if you have a medical condition. Your medical cover ceases once you retire. Unless you are in perfect health, coverage is questionable.

Stay Healthy

The best way to manage healthcare costs is to stay in the pink of health. Exercise regularly, eat a healthier diet and go for a medical examination annually. Most importantly, educate yourself on health matters. The greatest form of wealth is health.

This article first appeared in the May 2014 issue of Financial Planning magazine published by the Financial Planning Association of Singapore (FPAS).