7 Key Steps in Financial Planning

Published June 2018

Written by Shawn Yap CFP & edited by ClearlySurely.com

Good financial planners are, in a sense, like doctors in preventive medicine.

This connection isn’t always intuitive but it is rather apt once we get to the heart of the matter.

Both are (supposed to be) professionals, and (again, supposed to) follow a set of standard of procedures for the people that seek their expertise.

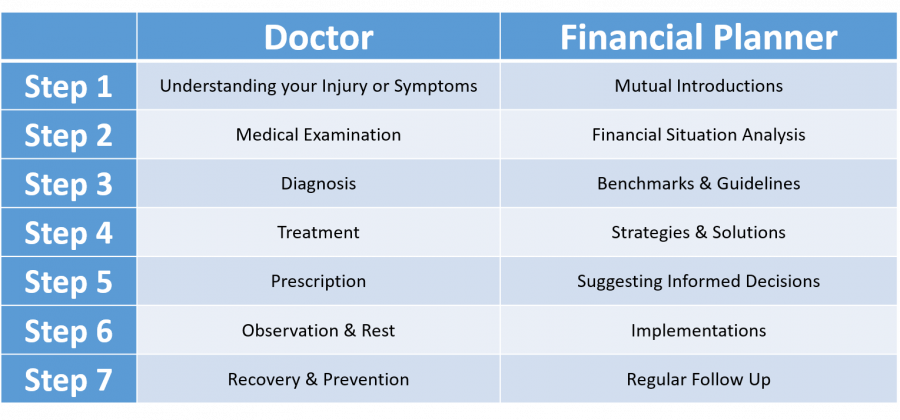

In a medical consultation, a patient would first describe the injury or symptoms, followed by a medical examination. The doctor would then make a diagnosis and prescribe the medication. Either the doctor would suggest a follow up or the patient would have recovered.

Turns out that Financial Planning works pretty much the same way. Here’s a quick side by side analysis:

The 7 Steps to Financial Nirvana (or close to it)

1) Mutual Introduction (Adviser & Client: 1 to 2 hours)

In this first meeting, both the client and the adviser would share more about themselves. The client would describe his concerns, goals & objectives while the adviser would explain how he works with clients and the necessary disclosures.

(Editor: At this stage, it is best to know if you are willing to be completely open with the adviser – they can only do their best work if they have all the information. Same as with describing your symptoms to any doctor, you shouldn’t leave anything out)

2) Financial Situation Analysis (Adviser: 1 to 2 hours or more depending on existing plans)

At this stage, client would provide information about his current financial situation and existing plans. The quality of advice depends on the information given by the client.

Whether the client’s objective is insurance planning, retirement planning or investment planning, the adviser will get to understand the client better with inputs from the client. Advisers are not mind readers! The client’s existing plans are also reviewed and analyzed together with the client’s overall situation.

3) Benchmarks & Guidelines (Adviser: 1 to 2 hours)

Steps 3 and 4 are the parts that clients don’t see, yet require the most work. The client’s financial position and goals are compared with international or local benchmarks and guidelines for planning. The adviser might also use proprietary models and financial software to evaluate the gap between the client’s current situation and his goals.

(Editor: Regardless of how the final numbers are obtained, it is important you understand them as a consumer – along with any of the key assumptions made)

4) Strategies & Solutions (Adviser: 2 to 4 hours)

The adviser starts to customize several strategies based on the client’s age, life stage, financial background and time horizon. They may also include budget and investment allocation.

A variety of products are then selected to build a portfolio for insurance or investment. Before the products are chosen, comparisons of similar products from different providers are done to find the most efficient and effective solutions.

5) Suggesting Informed Decisions (Adviser & Client: 1 to 3 hours)

Financial advisory is about helping clients to make a prudent decision and this inevitably involves some form of education to empower the client with financial wisdom.

The adviser would explain the whys and the hows and go through every option including the pros and cons with the client. After understanding and clarifying the different solutions, the client would have the choice to select and adjust the final strategy based on his preferences.

6) Implementation (Adviser & Client: 1 to 3 hours)

When all’s said – its time to roll up the sleeves and get to work.

Once the client has decided on the course of action, the adviser will assist the client with the tedious and occasionally mind-boggling administrative procedures, which include applications, appeals and amendments.

The implementation duration may range from several days for investment execution to several months for medical (and possibly financial) underwriting.

7) Follow Up

The old paradigm is that when you buy a product from an adviser, you expect the adviser to serve you for the rest of his (or your) life. As you can see, a good adviser does a lot of work.

The graceful swan you see on the lake is paddling hard underwater! The basic service to demand for insurance is claims support. For investments, the monitoring and management may be done by the adviser, financial institute or the client depending on the arrangement.

For fee-based advisers, there are two choices: one-time advice or continuous advice. Instead of buying financial products, sometimes randomly, to fulfil a specific purpose, prudent clients may prefer to enhance their overall wealth in a more disciplined and holistic manner.

Rome was not built in a day. It is not possible for the adviser to impart everything you need to know in a few sessions. By retaining a professional relationship with the right adviser over time, the adviser would understand you better in terms of financial habits (good and bad), investing style (reckless or overly conservative) and your personal mindset on money, which could be holding you back in protecting or enhancing your assets.

With a dedicated service, you can gain insights into your personal finance tailored to you. This is offered through a retainer to coach, educate and advise you on a quarterly, half yearly or yearly basis.

All in All

The whole advisory process takes about 3 to 4 meetings to complete.

On average, the adviser takes a total of 7 to 16 hours to finish the job – and that is a lot of coffee needed!

Still, the purpose of highlighting these steps is to provide a good overview of the actual amount of work and planning required for Financial planning, which should never be a rushed job.

This article was first published at Clearly Surely on 21st June 2018.