Not All Bonds Are Born Equal

Published May 2017

Written by Shawn Yap CFP

Compared to equities, bonds are often perceived to be a safer instrument. This may not be always the case.

A business has two common ways to raise funds: Sell company shares or borrow money in the form of loans. A shareholder has “ownership” of a company with rights to vote, participate in the change of the company’s value in terms of its share price and receive declared dividends. On the other hand, a bond holder is a creditor who lends money to a company for an interest at a rate which corresponds to the chance of default. A bond is the debt of a company where it pays an interest usually in the form of coupons to investors thereby widely known as a fixed income security.

Being a different instrument compared to equities, bonds are classified under a separate asset class for the purpose of diversifying your investment portfolio.

Types of Bond

Bonds can be issued by either corporations or governments (government bonds are also known as sovereign debts). They can be short or long term ranging from a couple of months to a few decades. Treasury bills (T-Bills) are bonds that mature in a year or less while perpetual bonds have no fixed maturity dates.

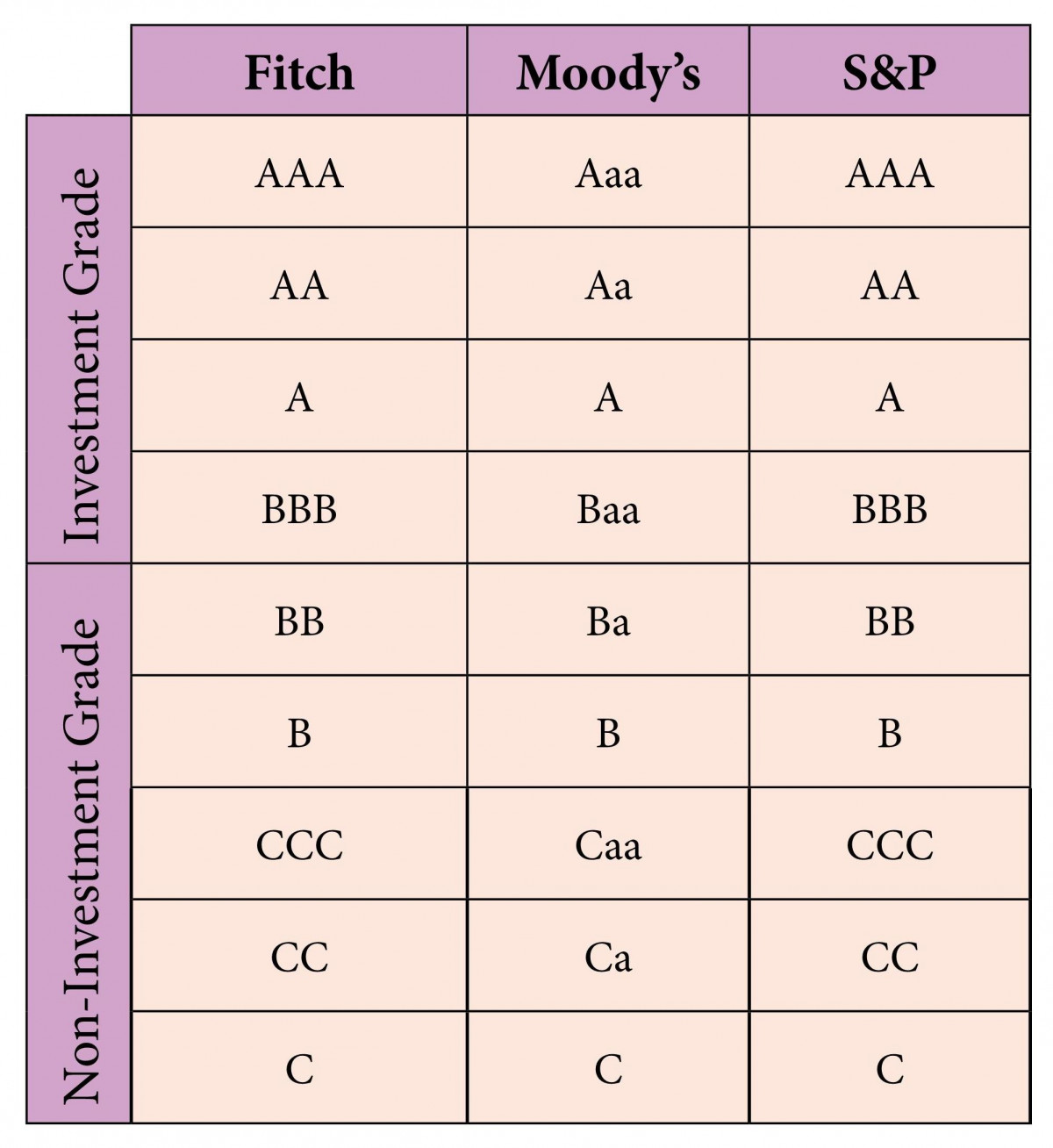

The quality of a bond can be ascertained through credit rating agencies such as S&P, Moody’s and Fitch popularly known as the Big Three. As with any rating system, the credit assessments are by no means a guarantee of performance. The two broad categories are Investment Grade and Non-Investment Grade. Other names for non-investment grade are High Yield, Junk and Speculative.

While the default rate for investment grade bonds is generally low, the default rate for non-investment grade bonds can vary from a single-digit to double-digit percentage. To increase the security of bonds, financial assets can be used for collateral. An example is a mortgage-backed bond which is collateralised with mortgage loans.

Risks to Note

The prices of bonds can fluctuate over time. Bond price has an inverse relationship with interest rate. When interest rate increases, bond price will decrease though short term bonds are less susceptible to interest rate changes than long term bonds. In addition, it is important to note that long term junk bonds have a higher correlation to equities.

Countries are rated for credit risk too. Emerging markets tend to have higher risks coupled with higher potential returns than developed nations. At this time of writing, the countries with the highest credit rating by the Big Three include Australia, Canada, Denmark, Germany, Norway, Singapore, Sweden and Switzerland. Although countries can default on their loans, it is very much less common than corporations. Nevertheless, some cash-rich companies can even be more credit worthy than entire countries.

The risk of currency exchange rate must also be considered and can be easily mitigated through diversification and hedging. In addition, please be cautious of holding both the bond and share of a single company. Even though bond holders rank higher than shareholders when it comes to company insolvency, it does not imply that the bond holder will get any capital back as the total liabilities can still exceed the total liquidated assets.

A bond is not always as safe as it sounds. Caveat Emptor!

This article first appeared under the title "Fixed Income Credit" in the May 2017 issue of Financial Planning magazine published by the Financial Planning Association of Singapore (FPAS).